FASB Crypto Fair Value: Measurement Levels Every Accountant Must Know

The way businesses measure and report crypto assets on their balance sheets changed significantly when the Financial Accounting Standards Board finalised its guidance requiring fair value accounting for certain digital assets. FASB crypto fair value rules, codified under ASC 350-60, replaced the old indefinite-lived intangible asset model that had frustrated preparers and auditors for years. Under the previous approach, companies could only write crypto holdings down when impaired but could never write them back up, even when market prices recovered sharply. The new model aligns carrying value with market reality by requiring entities to mark qualifying crypto assets to fair value at each reporting date, with unrealised gains and losses flowing through net income. For accounting firms advising corporate clients, and for CFOs managing treasury positions in Bitcoin or other digital assets, understanding how fair value is measured and classified is no longer optional. It is a core competency.

Why FASB Moved to Fair Value for Crypto Assets

The old impairment-only model was widely criticised as producing financial statements that understated asset values during bull markets and failed to give investors a current picture of a company's economic position. A company that bought Bitcoin at a high price, watched it fall, took an impairment charge, and then held through a recovery would carry the asset at the impaired value indefinitely. That asymmetry made balance sheets misleading. FASB responded after years of stakeholder feedback by issuing an update requiring fair value measurement for in-scope crypto assets, with changes in fair value recognised in net income each period. The standard applies to assets that meet specific criteria: they must be intangible assets, secured through cryptography, reside on a distributed ledger, and not give the holder a claim on underlying goods, services, or another asset. Assets that do not meet those criteria, including certain utility tokens and non-fungible tokens, fall outside the scope and require separate accounting analysis. This scoping decision matters enormously for firms onboarding clients with diverse digital asset portfolios.

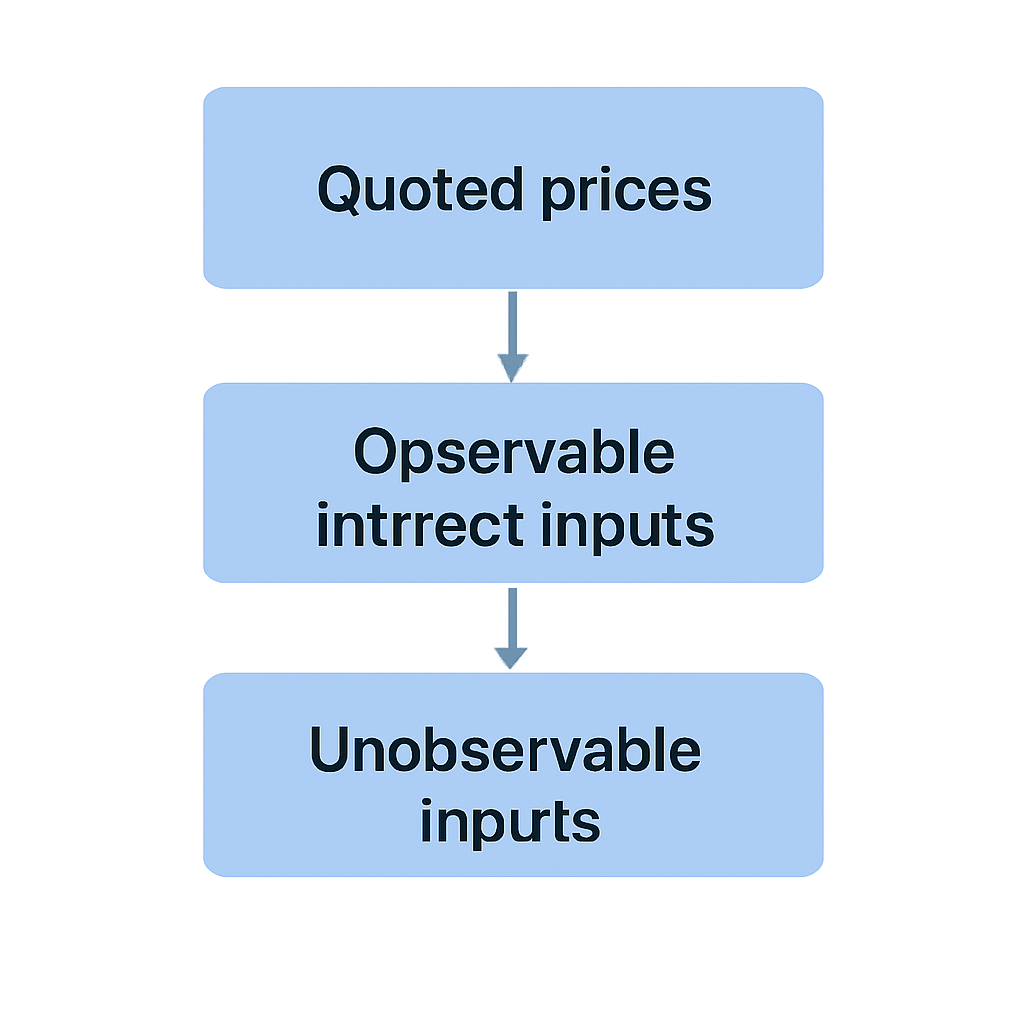

The FASB Fair Value Hierarchy: Level 1, Level 2, and Level 3 Inputs

Fair value under US GAAP is not a single number dropped from the sky. It is derived through a structured hierarchy that prioritises the most reliable evidence. ASC 820, the master fair value standard, establishes three levels of inputs, and those same levels apply when measuring crypto assets under ASC 350-60 crypto guidance. Understanding where a particular asset sits in this hierarchy determines how auditable and defensible the reported figure will be.

The table below summarises the three levels and their application to common crypto asset types.

Three Levels of Inputs

| Level | Input Type | Typical Crypto Asset Examples | Audit Risk |

|---|---|---|---|

| Level 1 | Quoted prices in active markets for identical assets | Bitcoin (BTC), Ether (ETH) on major exchanges | Low |

| Level 2 | Observable inputs other than Level 1 quoted prices | Less liquid tokens with observable but indirect pricing | Medium |

| Level 3 | Unobservable inputs based on entity assumptions | Illiquid or privately issued tokens, certain DeFi positions | High |

Level 1 Classification for Bitcoin and Ether

For most corporate treasuries holding Bitcoin or Ether, Level 1 classification is straightforward. There are active, liquid markets on multiple exchanges, and quoted prices are readily available. The measurement challenge intensifies quickly once a client holds tokens with thin trading volumes, assets locked in staking protocols, or positions in wrapped tokens where the peg introduces an additional variable. Those situations push preparers toward Level 2 or Level 3 territory, which requires more documentation, more judgment, and greater scrutiny from auditors.

ASC 350-60 Crypto: Scope, Recognition, and Disclosure Requirements

ASC 350-60 crypto guidance sets out not just how to measure crypto assets at fair value but also what disclosures must accompany those measurements. Entities must disclose the significant inputs and valuation techniques used for Level 2 and Level 3 measurements, which can be a significant documentation undertaking for firms holding a heterogeneous portfolio. For Level 3 assets, a reconciliation of the opening and closing balance is required, including the impact of unrealised gains and losses for the period. These requirements are not trivial. A client holding a basket of twenty tokens, several of which trade on decentralised exchanges with limited price transparency, will need a robust valuation process before period-end close.

Disclosure Requirements for Level 2 and Level 3

The recognition mechanics are equally important. Under ASC 350-60, gains and losses arising from fair value changes are recognised in net income, not in other comprehensive income. This means that a company with a large Bitcoin position will see its reported earnings fluctuate with crypto price movements, a consideration that has material implications for earnings-per-share calculations, debt covenant compliance, and investor communications. Accounting advisers need to help clients model these income statement effects before they become surprises at year-end.

Gains and Losses in Net Income

| Disclosure Requirement | Applies To | Notes |

|---|---|---|

| Significant holdings description | All in-scope crypto assets | Name, units held, fair value at period-end |

| Valuation technique and inputs | Level 2 and Level 3 assets | Must describe methodology used |

| Level 3 rollforward | Level 3 assets only | Opening balance, purchases, sales, gains, losses, closing balance |

| Unrealised gains and losses | All in-scope crypto assets | Separately disclosed for assets held at period-end |

| Restrictions on assets | Where applicable | Includes lock-up periods, staking restrictions |

How IFRS Crypto Assets Treatment Compares to US GAAP

For firms with multinational clients or those preparing consolidated statements that span jurisdictions, understanding the gap between US GAAP and IFRS crypto assets treatment is essential. IFRS does not yet have a dedicated crypto asset standard equivalent to ASC 350-60. The IASB published a narrow-scope amendment in 2023 clarifying that crypto assets meeting the definition of an intangible asset under IAS 38 must generally be carried under either the cost model or the revaluation model. Under the revaluation model, upward revaluations go to other comprehensive income rather than profit or loss, which is a fundamental difference from the US GAAP approach where all fair value movements hit net income.

Scoping Analysis for Crypto Under IFRS

Crypto IFRS accounting also requires careful scoping analysis. Holdings of a stablecoin that is contractually redeemable for cash may qualify as a financial asset under IFRS 9, bringing it within the fair value through profit or loss model that more closely resembles the ASC 350-60 outcome. But a volatile utility token is more likely to be an intangible asset under IAS 38, with measurement choices that differ materially from the FASB model. Firms advising clients who report under both frameworks need to maintain parallel accounting policies and document the reconciling differences clearly. A well-maintained crypto sub-ledger and cost basis reconciliation system is the practical foundation for managing this complexity.

| Feature | US GAAP (ASC 350-60) | IFRS (IAS 38 / IFRS 9) |

|---|---|---|

| Primary standard | ASC 350-60 (specific crypto guidance) | IAS 38 or IFRS 9 (no dedicated crypto standard) |

| Measurement basis | Fair value mandatory for in-scope assets | Cost or revaluation model (IAS 38); FVTPL possible under IFRS 9 |

| Gains and losses recognition | Net income (P&L) | OCI (revaluation model) or P&L (IFRS 9 FVTPL) |

| Impairment testing | Not required under fair value model | Required under cost model (IAS 36) |

| Dedicated guidance | Yes | No (IASB narrow-scope amendment only) |

Staking, Wrapping, and DeFi: Measurement Complications

The fair value hierarchy becomes considerably more complex when clients hold crypto assets in forms other than simple spot positions on centralised exchanges. Staked assets present a particular challenge. When a token is locked in a staking protocol, the holder may face a delay before the asset can be unlocked and sold. That restriction on liquidity is a relevant factor under ASC 820's principal market concept, and it may warrant an adjustment to the quoted price or a shift from Level 1 to Level 2 classification. Wrapped tokens add another layer. A wrapped version of an asset trades on a different chain and relies on a bridge mechanism to maintain its peg. If the peg has historically deviated or if the bridge carries smart contract risk, a straightforward mapping to the underlying token's price may not represent fair value accurately.

DeFi Liquidity Pool Measurement Challenges

DeFi liquidity pool positions are arguably the most difficult to measure. A position in an automated market maker pool is not a simple token holding. It is a proportional claim on two or more assets, subject to impermanent loss dynamics, and there is no single quoted price for such a position on any exchange. Firms advising clients with DeFi exposure need valuation methodologies that can withstand audit scrutiny, and those methodologies must be documented and applied consistently period over period. The interaction of these measurement questions with emerging reporting regimes such as CARF crypto reporting and DAC8 reporting, which focus on transaction-level data rather than balance sheet values, creates a layered compliance environment that demands systematic tooling.

Audit Readiness and the Role of Sub-Ledger Data

Fair value measurement under ASC 350-60 is only as good as the underlying data. Auditors reviewing a crypto-holding client will want to trace each position from its acquisition through to the period-end fair value figure. That trace depends on having complete, timestamped transaction records tied to the specific wallets and exchange accounts where assets are held. Gaps in the data trail, such as unmapped wallet addresses, missing exchange API feeds, or unreconciled transfers between custodians, create audit findings that can delay sign-off and damage client relationships.

Sub-Ledger Infrastructure for Audit Readiness

Accounting firms that have invested in sub-ledger infrastructure capable of pulling transaction data from exchanges, wallets, and on-chain sources, and mapping each holding to its appropriate fair value level, are in a materially stronger position than those relying on manual spreadsheets. The sub-ledger also needs to capture cost basis data correctly, because even under the fair value model, cost basis remains relevant for tax purposes under crypto US GAAP accounting and for reconciling book-to-tax differences. Clients that separate their financial reporting system from their tax cost basis tracking create unnecessary reconciliation work and increase the risk of errors in both sets of records.

Illustrative Scenario

To illustrate how this applies in practice, consider the following scenario:

Michael is a Senior Manager at a mid-sized US accounting firm that recently added three corporate clients with material crypto holdings to its portfolio. One client holds only Bitcoin and Ether on a regulated custodian, making Level 1 fair value measurement straightforward. A second client holds a mix of Bitcoin, a lower-liquidity altcoin, and a position staked in an Ethereum validator, which requires Level 1 classification for the Bitcoin, Level 2 analysis for the altcoin, and a valuation judgment call for the staked position given the unbonding period. The third client holds a liquidity pool position on a DeFi protocol, requiring a bespoke valuation model that neither the client nor Michael's firm had previously built.

Michael's team uses CryptaCount to pull complete transaction histories across all three clients, map each holding to the correct fair value level, and generate the disclosure schedules required under ASC 350-60, including the Level 3 rollforward for the DeFi position. What previously would have taken weeks of manual reconciliation across spreadsheets is completed before the audit fieldwork begins. The auditors receive a clean, traceable data package, and all three clients sign off on time. Michael's firm subsequently positions the fair value advisory work as a standalone service offering for new corporate crypto clients.

Frequently Asked Questions

What is FASB crypto fair value and when did it become effective?

FASB crypto fair value refers to the requirement under ASC 350-60 for entities to measure qualifying crypto assets at fair value at each reporting date, with changes recognised in net income. The standard became effective for fiscal years beginning after December 15, 2024, with early adoption permitted. It replaced the impairment-only model that had applied under the indefinite-lived intangible asset framework.

Which crypto assets are in scope for ASC 350-60?

ASC 350-60 covers intangible assets that are secured through cryptography, reside on a blockchain or distributed ledger, and do not give the holder a contractual claim on underlying goods, services, or financial assets. Bitcoin and Ether are the most commonly cited in-scope assets. Non-fungible tokens and certain utility tokens may fall outside the scope and require separate accounting analysis.

How does the fair value hierarchy apply to crypto assets under US GAAP?

The ASC 820 fair value hierarchy applies directly to crypto asset measurement. Level 1 uses quoted prices from active markets, which applies to liquid assets like Bitcoin traded on major exchanges. Level 2 relies on observable but indirect inputs for less liquid tokens. Level 3 uses entity-developed assumptions for illiquid or structurally complex positions such as DeFi liquidity pool stakes.

What is the key difference between ASC 350-60 crypto and IFRS crypto assets treatment?

Under ASC 350-60, fair value is mandatory for in-scope assets and all gains and losses flow through net income. IFRS does not have a dedicated crypto standard, so assets are typically assessed under IAS 38 as intangible assets, where the revaluation model routes gains through other comprehensive income rather than profit or loss. This produces different earnings volatility profiles for the same underlying asset.

Does crypto IFRS accounting require fair value measurement?

IFRS does not mandate fair value for crypto assets the way ASC 350-60 does under US GAAP. Under IAS 38, entities choose between the cost model and the revaluation model. If a crypto asset qualifies as a financial asset under IFRS 9, fair value through profit or loss accounting becomes available, producing an outcome closer to the US GAAP treatment. The classification decision requires careful analysis of the asset's contractual terms.

How should staked crypto assets be measured at fair value?

Staked assets that cannot be immediately sold due to lock-up or unbonding periods may warrant a discount to the quoted spot price, or reclassification from Level 1 to Level 2 in the fair value hierarchy, to reflect the liquidity restriction. The specific treatment depends on the length of the restriction, the market for the asset, and the entity's own accounting policy, all of which should be documented and applied consistently.

What disclosures are required under ASC 350-60 for crypto assets?

Entities must disclose the name and quantity of each significant crypto holding along with its period-end fair value, the valuation techniques and inputs used for Level 2 and Level 3 assets, a rollforward of Level 3 balances, and unrealised gains and losses for the period. Restrictions on assets, such as staking lock-ups, must also be disclosed where applicable. These requirements apply at each annual and interim reporting date.

How do CARF and DAC8 reporting obligations relate to fair value accounting?

CARF crypto reporting and DAC8 reporting are transaction-level regulatory reporting regimes that require crypto asset service providers to report client transaction data to tax authorities. They operate separately from balance sheet fair value accounting under ASC 350-60 or IFRS. However, the transaction data collected for CARF and DAC8 purposes is the same underlying data needed to support fair value measurement and cost basis tracking, so integrated data infrastructure serves both purposes.

Can an accounting firm use sub-ledger software to automate ASC 350-60 compliance?

Yes. Sub-ledger software that connects to exchange APIs, wallet addresses, and on-chain data sources can automate the collection of transaction records, map each position to the correct fair value level, and generate the disclosure schedules required under ASC 350-60. This reduces manual reconciliation effort, improves audit traceability, and allows firms to scale crypto accounting services across multiple clients efficiently.

Source: CryptaCount