IMF: Tokenization Could Reshape Settlement but Fragments Without Coordinated Standards

The International Monetary Fund has issued one of its most direct statements yet on blockchain-based finance: tokenization holds genuine potential to compress multi-day settlement cycles into near-instant transactions, but without coordinated standards across jurisdictions it could instead generate new and unfamiliar sources of systemic risk. For accounting firms, auditors and CFOs advising on digital asset strategy, this signals that the regulatory environment around tokenized markets is actively forming, and that positioning now matters.

What the IMF Actually Said

Writing in an IMF blog published on 2 July 2026, Tobias Adrian, the Fund's Financial Counsellor and Director of the Monetary and Capital Markets Department, argued that tokenization is no longer a peripheral crypto phenomenon. Placing assets, settlement processes and recordkeeping onto a shared ledger infrastructure has the potential to fundamentally alter how financial markets function.

Settlement compression as the core efficiency case

The central operational argument is straightforward. Traditional securities markets run on settlement cycles that can span several business days. A tokenized equivalent, where ownership transfer and payment happen atomically on the same ledger, collapses that window dramatically. Adrian framed this as more than an incremental improvement: the architecture itself changes, removing the layers of reconciliation, nostro-vostro funding and counterparty waiting risk that sit between trade execution and final settlement today.

Risk migration, not risk elimination

The IMF's caution is equally pointed. Tokenization does not remove risk from the system; it relocates it. Under conventional market structure, intermediaries such as custodians, clearing houses and correspondent banks absorb and manage a range of operational and counterparty exposures. When that function shifts to shared ledger infrastructure, the risk concentrates in smart contracts, distributed ledger protocols and third-party technology service providers. These are entities that currently sit outside many of the prudential frameworks designed for traditional financial institutions. Governance failures, protocol bugs or outages at critical infrastructure nodes could therefore propagate losses in ways that existing resolution and recovery regimes were not designed to handle.

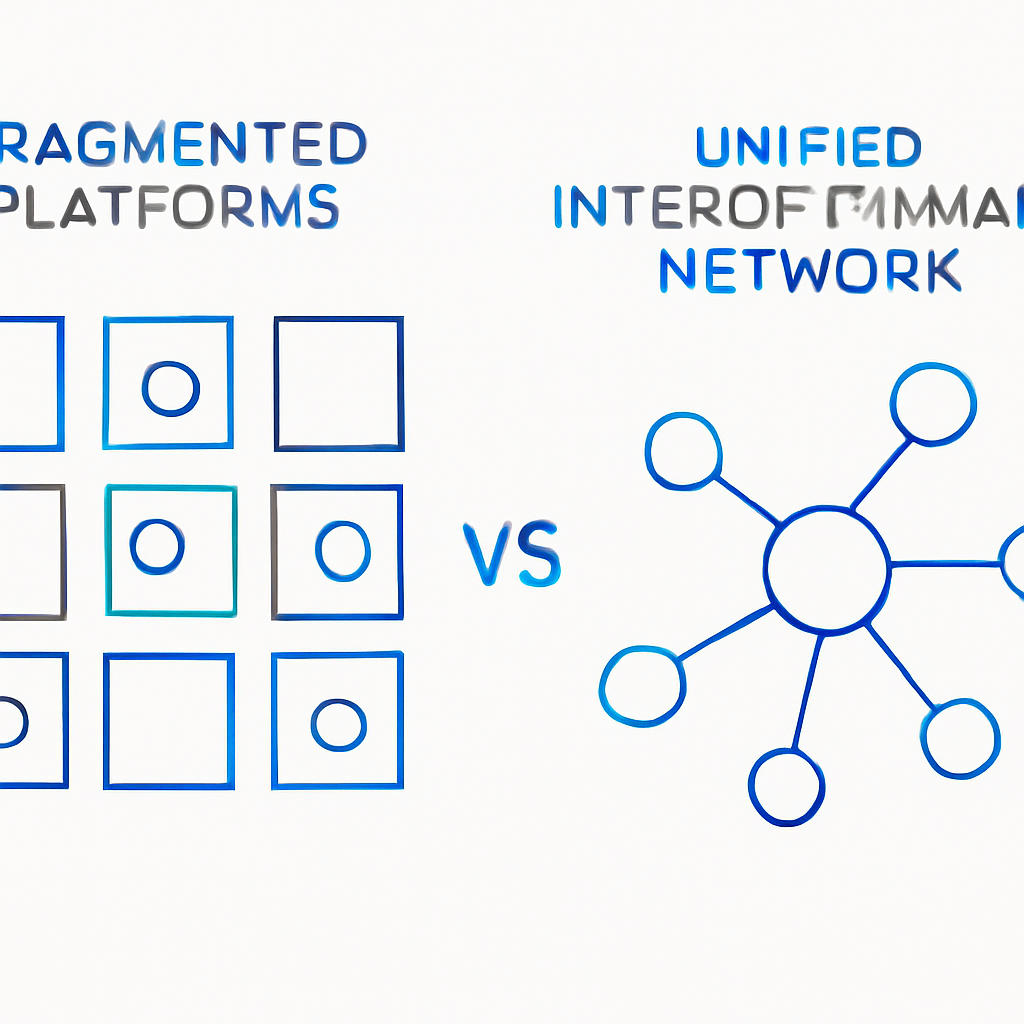

The Fragmentation Problem

The IMF's most pointed structural warning concerns interoperability. Tokenized markets are currently developing across a range of platforms and networks that do not share common technical or legal standards. If that trajectory continues, the financial system risks ending up with multiple tokenized silos, each operating on incompatible infrastructure. Transactions that currently flow seamlessly through globally interconnected correspondent banking and clearing networks could become technically stranded when they need to cross from one tokenized platform to another.

Why fragmentation is a systemic concern, not just an efficiency one

Fragmented tokenized markets would create asymmetric liquidity pools. In a stress scenario, assets held on one platform that cannot be readily liquidated or transferred to another could amplify price dislocations. The IMF's framing is that decisions made now on settlement assets, governance models, interoperability protocols and the role of central bank money in settlement will shape whether tokenization strengthens or weakens overall financial stability. That window, Adrian argued, is narrow.

The Regulatory Landscape Taking Shape

The IMF's analysis sits alongside active regulatory movement in several major jurisdictions. In the United States, the Securities and Exchange Commission has been working through how existing securities laws map onto tokenized assets rather than constructing an entirely separate framework. The agency has also signalled openness to sandbox arrangements that would allow market participants to test blockchain-based trading platforms for tokenized securities while a longer-term rulebook is developed.

Separately, major financial institutions are accelerating their own preparations. A consortium whose shareholders reportedly include JPMorgan Chase, Bank of America and Barclays has been reported to be planning a tokenized deposit network targeting a launch in early 2027, designed to keep deposits within the regulated banking system while enabling programmable, faster payment flows. This is a practical example of the institutional momentum the IMF is both acknowledging and cautioning about.

For EU-based firms, the interplay between tokenization infrastructure and existing frameworks such as MiCA authorization requirements now in force for crypto-asset service providers is already live. How tokenized securities, deposits and funds map onto MiCA, MiFID II, EMIR and settlement finality rules remains an open question that regulators are working through in real time.

Implications for Firms Advising on Digital Assets

The IMF's framing has practical consequences for accounting, audit and advisory practices. Several points stand out.

Accounting and audit exposure points

First, the migration of settlement risk toward smart contract and ledger infrastructure raises questions about how operational risk is identified, measured and disclosed in financial statements. Current risk disclosures in annual reports and interim accounts were written for intermediary-centric market structures. Auditors assessing tokenized asset exposures need frameworks that capture technology concentration risk, protocol governance risk and the absence of conventional resolution mechanisms.

Second, fair value measurement of tokenized assets where secondary market liquidity is thin or fragmented across incompatible platforms is a live accounting challenge. IFRS 13 and ASC 820 hierarchies were not designed with atomised, platform-specific liquidity in mind.

Third, firms need to monitor how settlement finality is legally defined for tokenized transactions in each jurisdiction. Settlement finality has direct consequences for derecognition of financial assets and liabilities under both IFRS 9 and US GAAP.

On the compliance side, the IMF's call for coordinated standards reinforces the importance of how clearing preparedness is being stress-tested across tokenized and traditional markets, particularly as regulators begin to extend oversight frameworks to tokenized market infrastructure.

Frequently Asked Questions

What is the IMF's core argument about tokenization and settlement?

The IMF argues that by placing assets, settlement and recordkeeping on a shared ledger, tokenization could replace multi-day settlement cycles with near-instant finality. However, it also cautions that this shifts operational and systemic risk away from traditional intermediaries and toward the underlying technology infrastructure, which is not yet covered by equivalent prudential regulation.

Why does the IMF treat fragmented tokenized platforms as a systemic risk?

If tokenized markets develop on incompatible platforms without common standards, liquidity becomes siloed. In a stress scenario, assets stranded on one network that cannot interact with another could amplify dislocations rather than absorbing them, creating new transmission channels for financial instability.

How does this affect accounting treatment of tokenized assets?

Settlement finality under tokenized infrastructure has direct implications for derecognition under IFRS 9 and ASC 820 fair value measurement where platform-specific liquidity is thin. Firms should also reconsider how operational risk disclosures capture smart contract and protocol governance exposures that existing frameworks were not designed to address.

What is the SEC doing on tokenized securities in the US?

According to the IMF blog and related reporting, the SEC has been mapping existing securities laws onto tokenized assets rather than building a separate regime. It has also indicated openness to sandbox arrangements allowing market participants to test blockchain-based trading platforms for tokenized securities while a more permanent framework is developed.

What should firms monitor in the near term?

Firms should track regulatory decisions on settlement assets, interoperability standards and the role of central bank digital infrastructure in tokenized settlement. The IMF explicitly framed these as decisions with a narrow window that will determine whether tokenization improves or complicates financial stability.

Source: Cointelegraph